Our Site uses cookies to improve your experience on our website. For more details, please read our Cookie Policy.

By closing this message or starting to navigate on this website, you agree to our use of cookies.

Our Site uses cookies to improve your experience on our website. For more details, please read our Cookie Policy.

By closing this message or starting to navigate on this website, you agree to our use of cookies.

This page is translated using machine translation. Please note that the content may not be 100% accurate.

Contact

Mitsui Fudosan Realty can provide a wide range of real estate services on both investment and residential properties.

Please feel free to give us a call or contact with mail inquiry.

Phone(English Line)

Contact Information by Region

- China400-120-1319

- HongKong800-93-3060

- Taiwan00801-81-2728

- Japan(English)0120-923-431

- Other Regions+81-3-6758-4072

Contact

Mitsui Fudosan Realty can provide a wide range of real estate services on both investment and residential properties.

Please feel free to give us a call or contact with mail inquiry.

Phone(English Line)

Contact Information by Region

- China400-120-1319

- HongKong800-93-3060

- Taiwan00801-81-2728

- Japan(English)0120-923-431

- Other Regions+81-3-6758-4072

This page is translated using machine translation. Please note that the content may not be 100% accurate.

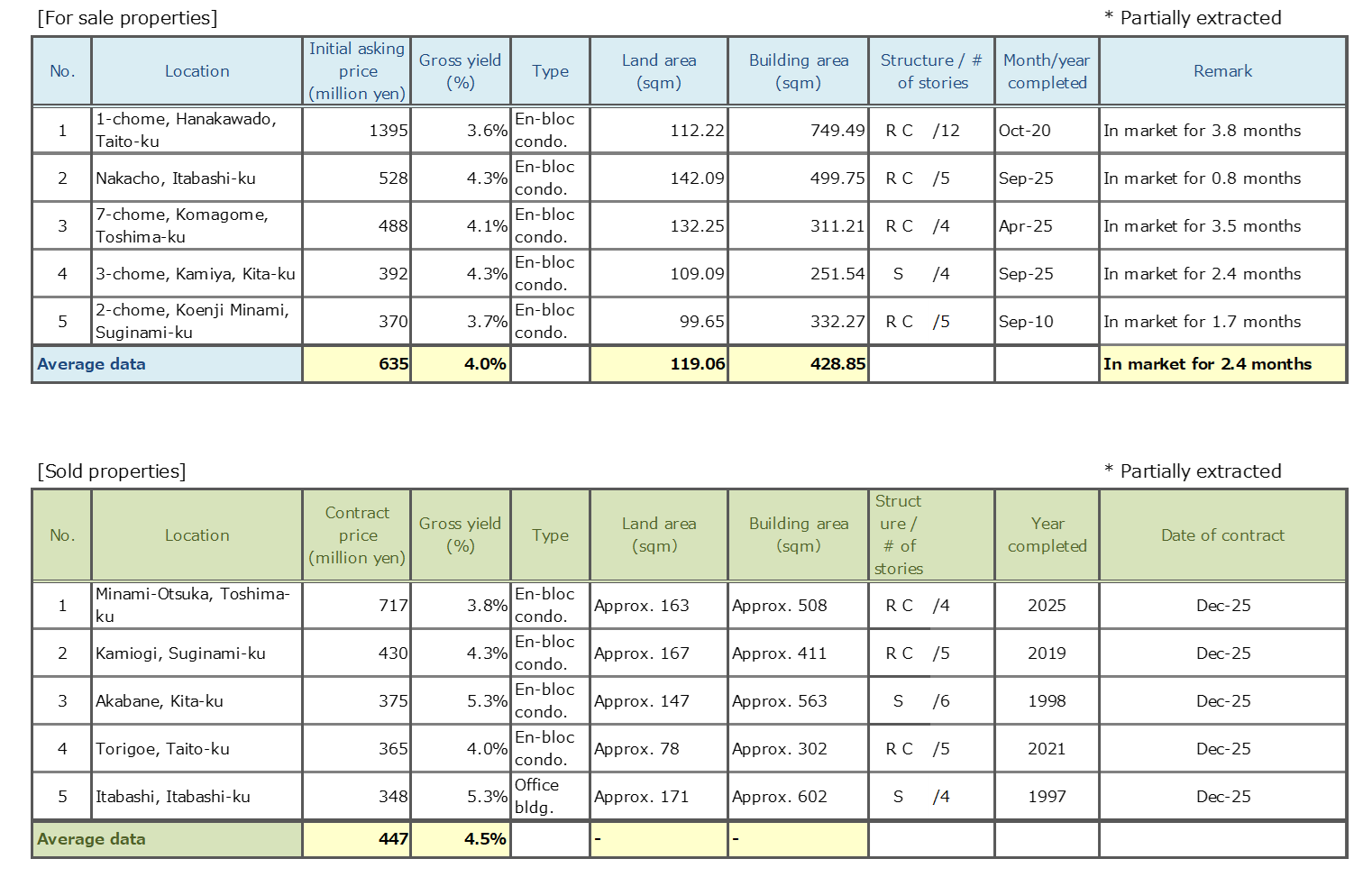

Investment Real Estate Market Report | 3Q FY2025

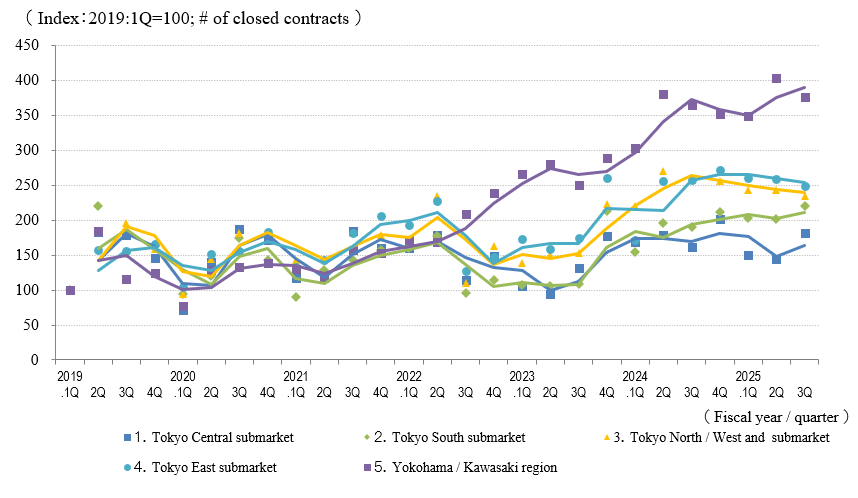

Areas subject to collection of data

Tokyo Central submarket: Minato-ku, Chiyoda-ku, Chuo-ku, Shibuya-ku, Shinjuku-ku, and Bunkyo-ku

Tokyo South submarket: Shinagawa-ku, Meguro-ku, Setagaya-ku, and Ota-ku

Tokyo North / West submarket: Suginami-ku, Nakano-ku, Nerima-ku, Toshima-ku, Itabashi-ku, Kita-ku, and Taito-ku

Tokyo East submarket: Koto-ku, Sumida-ku, Arakawa-ku, Edogawa-ku, Katsushika-ku, and Adachi-ku

Yokohama / Kawasaki region: Yokohama city and Kawasaki city

Detailed descriptions

Pick Up Area: For investment real estate, trends in the average gross yields on contract price and initial asking price, together with the number of closed contracts by submarkets are represented in the graph. The details of the transition of actual market value and properties both for sale and sold in certain neighborhoods are also shown.

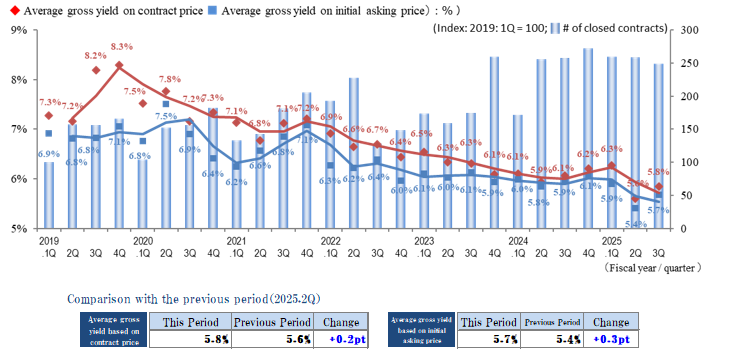

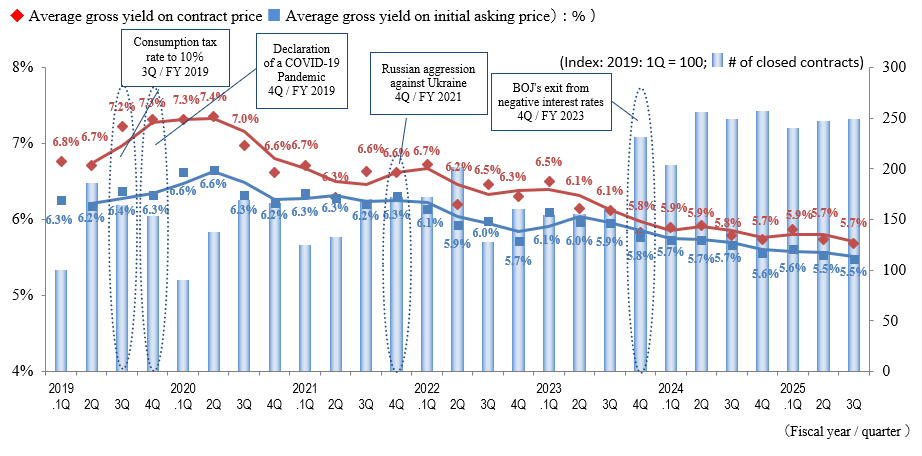

Market Overview: As an overview of all the submarkets, the trend from the past to this quarter is available. Trends in the average gross yields based on contract price and initial asking price together with the number of closed contracts by area are shown for comparison.

Data Source: Information is extracted from the database containing properties offered for sale and contracts concluded through Mitsui Fudosan Realty Network (En-bloc condominiums / office buildings / apartment buildings).

- Number of Transactions & Average Gross Yield on Contract Price: Number of contracts closed in a quarter (three months) and average gross yield of them (including estimated values)

- Average Gross Yield on Initial Asking Price: Quarterly average gross yield of closed contracts based on their asking price initially quoted

*Figures in each chart represent indices based on values for 1Q / FY2019 set at 100.

(Average Gross Yield on Contract Price is shown as an index to Average Gross Yield on Initial Asking Price for 1Q / FY 2019 set at 100.)

[Note] The historical data may be revised subsequently due to maintenance carried out from time to time, such as adding newly acquired data.

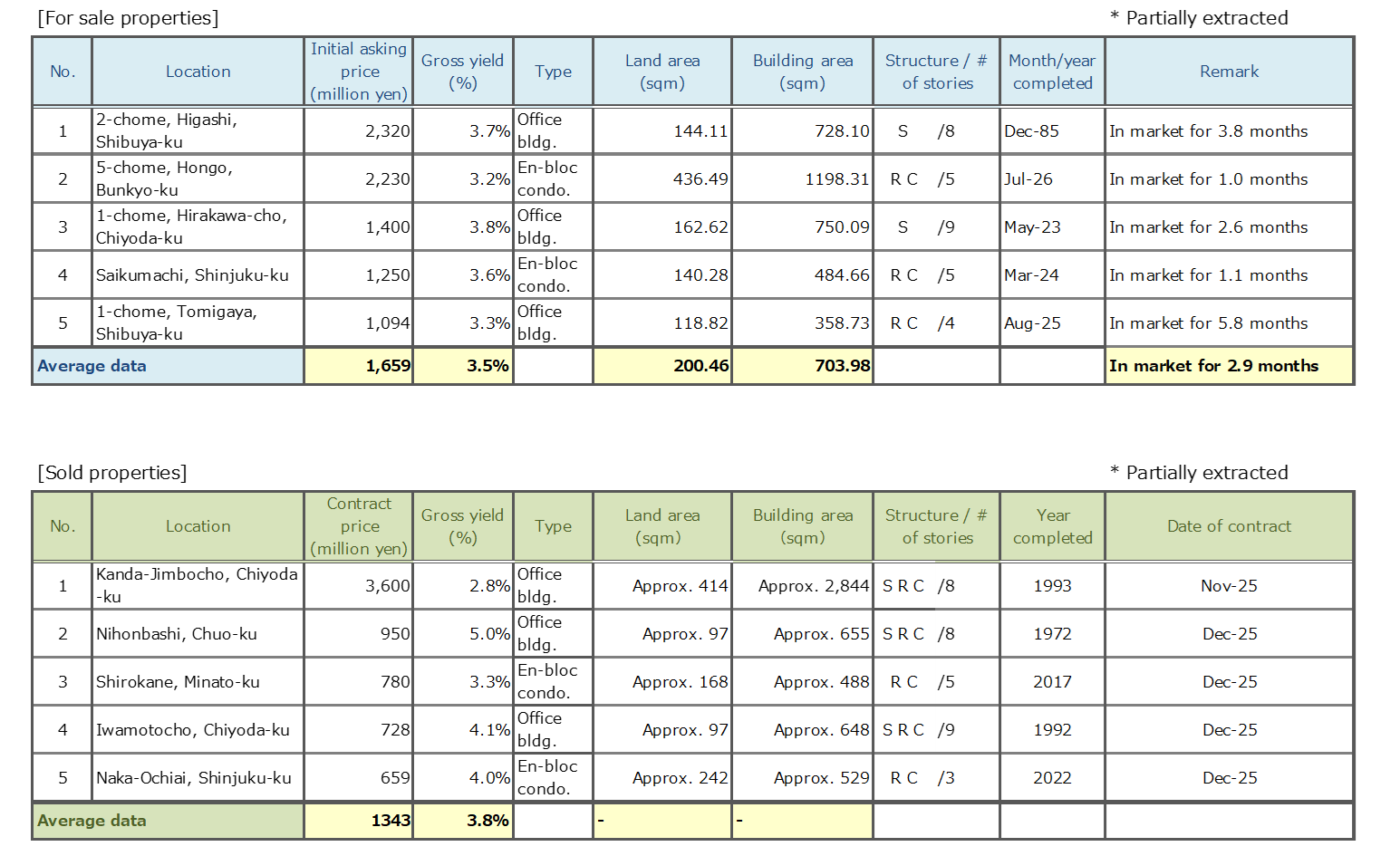

Pick Up Area -Tokyo Central submarket-

(*)Tokyo Central submarket: Minato-ku, Chiyoda-ku, Chuo-ku, Shibuya-ku, Shinjuku-ku, and Bunkyo-ku

◆Movements by Quarter: Average Gross Yield on Contract Price / Average Gross Yield on Initial Asking Price / Number of Transactions

◆Brokered Transactions of Investment Real Estate in the Submarket

The indices of the average gross yield on the initial asking price and on the contract price were down by 0.2 points and 0.3 points quarter over quarter (QoQ) (prices rose), respectively, in the Tokyo Central submarket in 3Q of FY 2025, while the number of contracts made increased YoY. However, since this includes multiple properties contracted at low yields, conceivably for purposes of vacating and redevelopment instead of yields, the decreasing trend in yields warrants further monitoring.

The leasing market in the Tokyo Central submarket is reviewed below:

■ Residences: The gentle increasing trend in rents continued. The trend toward conclusion of contracts at particularly high prices on residences with floor areas of more than 100 sqm and those with parking facilities has been pronounced since last year.

■ Offices: The trends toward lower vacancy rates and higher rents continued for both new and existing supplies, centered on large-scale office buildings, amid continued booming demand from the corporate need for improved office environments and locations to secure human resources.

■ Retail: Inbound consumption remains favorable, backed by such factors as continuing record high numbers of visitors to Japan from abroad. While rents remained in an increasing trend centered on street-level shops in well-known areas of the Tokyo Central submarket, the pace was slow.

As the aforementioned favorable conditions continue for each asset type in the leasing market, the risk factors include the rising costs of ownership as a result of interest-rate hikes and the rising costs of maintenance, including repairs, due to higher construction and labor costs. Accordingly, to maintain or increase effective yields, property owners will need to increase rents in excess of the increase in the costs of ownership. Another concern is the potential for a decrease in tax savings from real estate due to revisions to the tax system. The impacts of these factors require verification for the conditions of property owners and individual property holdings. Feel free to contact us with any concerns.

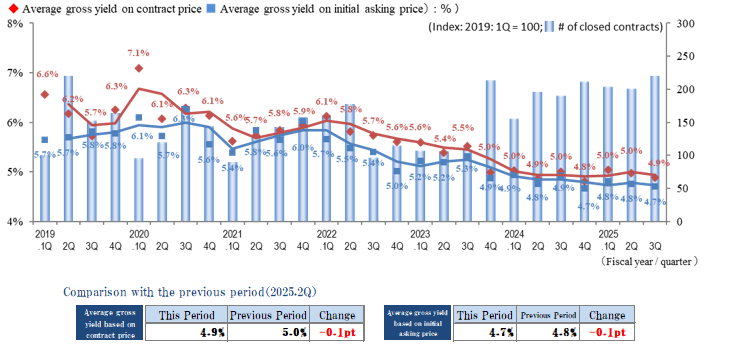

Pick Up Area -Tokyo South submarket-

(*) Tokyo South submarket: Shinagawa-ku, Meguro-ku, Setagaya-ku, and Ota-ku

◆Movements by Quarter: Average Gross Yield on Contract Price / Average Gross Yield on Initial Asking Price / Number of Transactions

◆Brokered Transactions of Investment Real Estate in the Submarket

The indices of the average gross yield on the initial asking price and on the contract price in the Tokyo South submarket in 3Q of FY 2025 were 4.7% (-0.1 points QoQ) and 4.9% (-0.1 points QoQ), respectively. A look at the trends over the most recent year shows that yields largely remain flat. While the number of contracts increased QoQ, the extent of the increase was limited because the number has remained at a similarly high level in each quarter over the past year. In addition, the difference between the indices of the average gross yield on the initial asking price and the contract price remained small. Since this state has continued since 4Q of FY 2023, based on transaction data the Tokyo South submarket can be said to remain stable.

The Bank of Japan monetary policy revisions in December brought the lengthy downward trend in yields to an end and led to increases in base interest rates for real estate lending. Continued rising construction costs are another factor behind rising prices, as continuing high labor and materials prices make it impractical to reduce prices of new properties. At the same time, demand for both residential and commercial properties remains steady in the Tokyo South submarket, and redevelopment plans in the Takanawa Gateway area and in Jiyugaoka are some factors supporting rising prices in this submarket. As such, market conditions that are relatively resistant to price decreases are expected to continue for now.

While there are concerns about buyer restraint due to rising interest rates, bullish pricing is expected to continue for newer properties and those in locations where supply is limited. Although stable transaction conditions are expected to continue for now, the need is increasing for investors to consider comprehensively such matters as property competitiveness, operating costs, and area potential instead of just profitability alone.

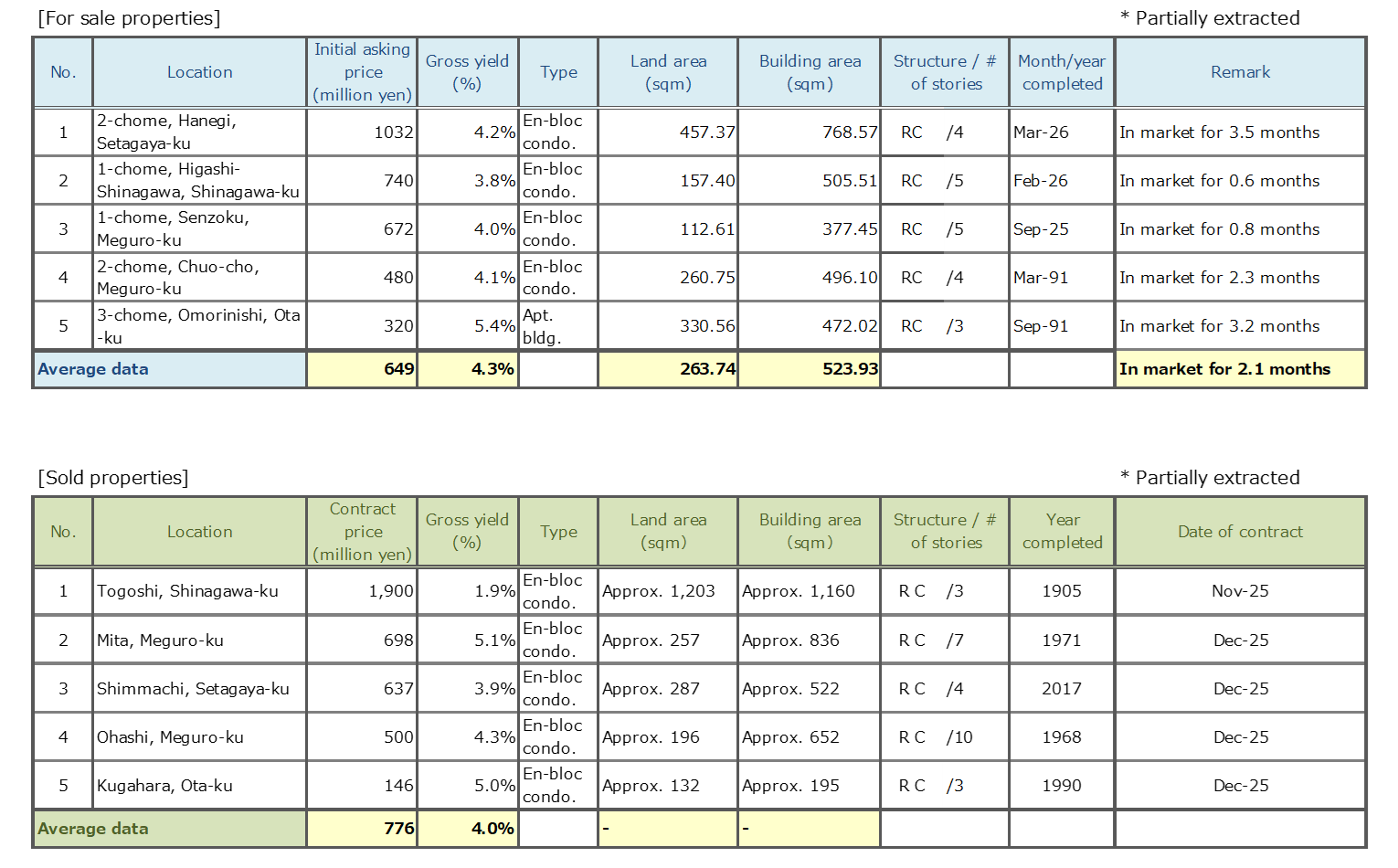

Pick Up Area -Tokyo North / West submarket-

(*) Tokyo North / West submarket: Suginami-ku, Nakano-ku, Nerima-ku, Toshima-ku, Itabashi-ku, Kita-ku, and Taito-ku

◆Movements by Quarter: Average Gross Yield on Contract Price / Average Gross Yield on Initial Asking Price / Number of Transactions

◆Brokered Transactions of Investment Real Estate in the Submarket

The indices of the average gross yield on the initial asking price and on the contract price in the Tokyo North / West submarket in 3Q of FY 2025 both increased from the previous quarter (2Q of FY 2025) as prices fell. Recent quarterly trends show that despite some variation, yields remain largely flat, with no major changes overall. While the number of contracts decreased QoQ, it is higher than it was a few years ago as trading remains active. On the other hand, buyers continue to focus on appropriate yields, and market polarization continues as properties with favorable conditions are highly liquid while more time is required to sell less competitive properties.

While sellers have various reasons for selling, it appears that they are increasingly choosing to sell to avoid worsening of earnings as a result of rising interest rates, in addition to the continuing trend toward securing gains. Since rising interest rates are leading to changes in budget plans of buyers planning to finance their purchases, it is becoming increasingly important to check bank interest rates, which are linked to short-term prime rates, in addition to real estate market conditions. It has been reported recently that the average price of a used condominium in Tokyo's 23 wards listed for sale in the last year was more than 100 million yen per 70 m2, but only properties near central Tokyo and those for which evaluation criteria, such as asset and profitability potential, are clear are benefiting from rising prices. Liquidity varies by area and property attributes, and it is essential to consider on an individual basis which points to emphasize in sale. Contact our specialized sections for more details.

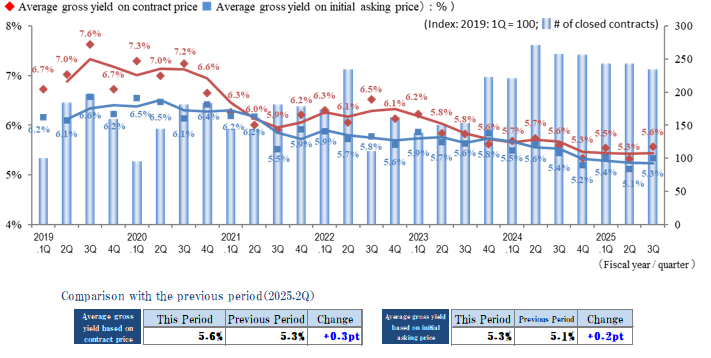

Pick Up Area -Tokyo East submarket-

(*) Tokyo East submarket: Koto-ku, Sumida-ku, Arakawa-ku, Edogawa-Ku, Katsushika-ku, and Adachi-ku

◆Movements by Quarter: Average Gross Yield on Contract Price / Average Gross Yield on Initial Asking Price / Number of Transactions

◆Brokered Transactions of Investment Real Estate in the Submarket

The yield index trends in the investment real estate market in the Tokyo East submarket showed a clear turning point in 3Q of FY 2025. The indices of the average gross yield on the contract price and on the initial asking price were 5.8% (up 0.2 points QoQ) and 5.7% (up 0.3 points QoQ), respectively, as yields increased (prices were adjusted). While rising prices drove yields down, centered on newer properties, in 2Q, this quarter's results seem to be affected by such factors as a stronger yield orientation among investors and an increase in transactions that involve price adjustments.

A look at transaction details in the submarket shows continued strong demand in areas near railway stations and planned for redevelopment with some cases where contracts were concluded even on properties with relatively low yields. At the same time, there is a clear trend toward market polarization, as older properties, such as those conforming to the old seismic standards and those with less convenient transportation access, need prices that can promise relatively higher yields. Also, in increasing numbers of cases, it takes some time for properties with optimistic asking prices to be sold, indicating that both sellers and buyers are looking at market levels closely. While judgments and decisions cannot be made based on results for this quarter alone, there is a possibility that the market as a whole is approaching a stage of adjustment away from past overheating, and it will be essential to continue to monitor transaction trends, including interest rate trends and the financial environment, going forward.

Pick Up Area -Yokohama / Kawasaki region-

(*) Yokohama and Kawasaki region: Yokohama city, Kawasaki city

◆Movements by Quarter: Average Gross Yield on Contract Price / Average Gross Yield on Initial Asking Price / Number of Transactions

◆Brokered Transactions of Investment Real Estate in the Submarket

The indices of the average gross yield on the initial asking price and on the contract price both decreased slightly (prices rose) in the Yokohama / Kawasaki region in 3Q of FY 2025. Yields appear to be relatively stable over the past year or two, after they had been decreasing since 2020. While the number of contracts decreased from 2Q, when it reached a record high since data collection began in 2017, the market remains active, and numerous transactions took place during 3Q.

While a certain number of customers are considering the Yokohama / Kawasaki region, where prices are relatively lower and yields can be expected to be higher than in the Tokyo Central submarket, the pronounced polarizing trend continues between the central and suburban areas in this region, and investors appear to be becoming increasingly cautious in the selection of investments, considering such factors as distances from railway stations and neighborhood conditions. In addition, while rent is in an increasing trend, in some cases even greater increases in construction costs are putting pressure on developers' business revenues and expenditures. Prices remain low on small-scale commercial sites in particular, which involve higher construction cost burdens. Even as stock prices continue to reach record highs, there are concerns about further interest rate hikes, and the future outlook for the real estate market remains uncertain. It will be essential to pay even closer attention to changing domestic and international monetary policy and economic conditions, such as exchange rates and stock prices.

General overview

◆Movements by Quarter: Average Gross Yield on Contract Price / Average Gross Yield on Initial Asking Price / Number of Transactions for the 5 Areas

◆Movements in Number of Transactions by Area

◆Movements in Average Gross Yield on Contract Price by Area

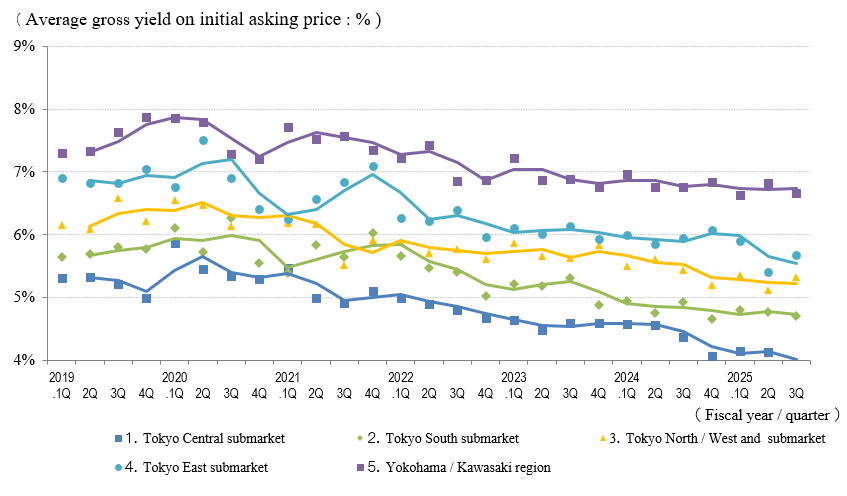

◆Movements in Average Gross Yield on Initial Asking Price by Area

While the numbers of transactions remained high overall in the investment real estate market in 3Q of FY 2025, there were some signs that the market was approaching a turning point. Although investors' appetite for investment remained steady, there were fewer signs of the uniform pricing seen previously, as investors became increasingly selective, focusing on properties' individual profitability and competitiveness.

In the Tokyo East submarket in particular, there was a pronounced increase in transactions involving price adjustments and yield increases. Backed by a stronger orientation toward yields, investors appear to be more conscious of profitability in making investment decisions in this submarket. At the same time, cases are apparent of contracts being concluded at relatively low yields on relatively more competitive properties and those in good locations as the differential in property evaluations is broadening. This trend suggests that the market as a whole is entering a phase of paying closer attention to quality.

External environmental factors, such as uncertainty about future monetary and fiscal policies and tax revisions following the latest election, in addition to interest rate trends associated with the Bank of Japan monetary policy changes, are impacting investors' state of mind. As a result of continued rising costs of property ownership and operation due to high construction and labor costs, it has become more important for investors to make decisions through close monitoring of such factors as effective yields and medium- to long-term profitability instead of just gross yields alone. Going forward, the above trend toward selectivity can be expected to spread to other submarkets, as prices will more strongly reflect factors such as property competitiveness and revenue structures. Although the market as a whole has not cooled dramatically, investor decision-making is becoming more sophisticated, and the quality of information, analytical capabilities, and timely decision-making are expected to remain strong contributing factors to investment results.