Our Site uses cookies to improve your experience on our website. For more details, please read our Cookie Policy.

By closing this message or starting to navigate on this website, you agree to our use of cookies.

Our Site uses cookies to improve your experience on our website. For more details, please read our Cookie Policy.

By closing this message or starting to navigate on this website, you agree to our use of cookies.

This page is translated using machine translation. Please note that the content may not be 100% accurate.

Contact

Mitsui Fudosan Realty can provide a wide range of real estate services on both investment and residential properties.

Please feel free to give us a call or contact with mail inquiry.

Phone(English Line)

Contact Information by Region

- China400-120-1319

- HongKong800-93-3060

- Taiwan00801-81-2728

- Japan(English)0120-923-431

- Other Regions+81-3-6758-4072

Contact

Mitsui Fudosan Realty can provide a wide range of real estate services on both investment and residential properties.

Please feel free to give us a call or contact with mail inquiry.

Phone(English Line)

Contact Information by Region

- China400-120-1319

- HongKong800-93-3060

- Taiwan00801-81-2728

- Japan(English)0120-923-431

- Other Regions+81-3-6758-4072

This page is translated using machine translation. Please note that the content may not be 100% accurate.

Investment Real Estate Market Report | 4Q FY2025

Areas subject to collection of data

Tokyo Central submarket: Minato-ku, Chiyoda-ku, Chuo-ku, Shibuya-ku, Shinjuku-ku, and Bunkyo-ku

Tokyo South submarket: Shinagawa-ku, Meguro-ku, Setagaya-ku, and Ota-ku

Tokyo North / West submarket: Suginami-ku, Nakano-ku, Nerima-ku, Toshima-ku, Itabashi-ku, Kita-ku, and Taito-ku

Tokyo East submarket: Koto-ku, Sumida-ku, Arakawa-ku, Edogawa-ku, Katsushika-ku, and Adachi-ku

Yokohama / Kawasaki region: Yokohama city and Kawasaki city

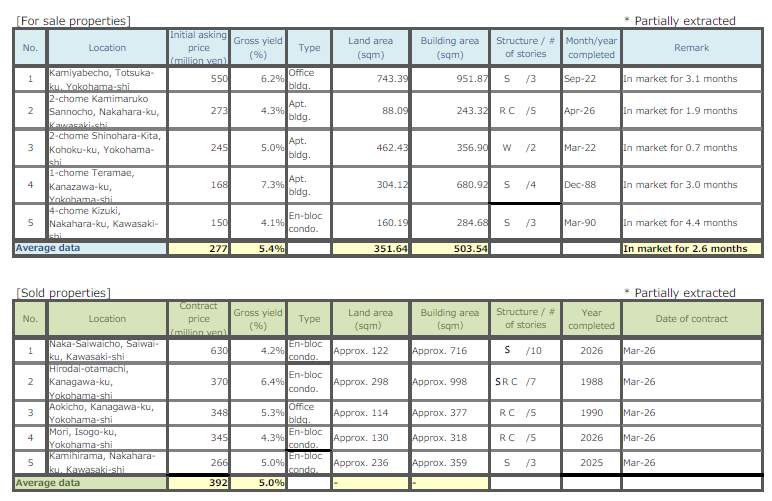

Detailed descriptions

Pick Up Area: For investment real estate, trends in the average gross yields on contract price and initial asking price, together with the number of closed contracts by submarkets are represented in the graph. The details of the transition of actual market value and properties both for sale and sold in certain neighborhoods are also shown.

Market Overview: As an overview of all the submarkets, the trend from the past to this quarter is available. Trends in the average gross yields based on contract price and initial asking price together with the number of closed contracts by area are shown for comparison.

Data Source: Information is extracted from the database containing properties offered for sale and contracts concluded through Mitsui Fudosan Realty Network (En-bloc condominiums / office buildings / apartment buildings).

- Number of Transactions & Average Gross Yield on Contract Price: Number of contracts closed in a quarter (three months) and average gross yield of them (including estimated values)

- Average Gross Yield on Initial Asking Price: Quarterly average gross yield of closed contracts based on their asking price initially quoted

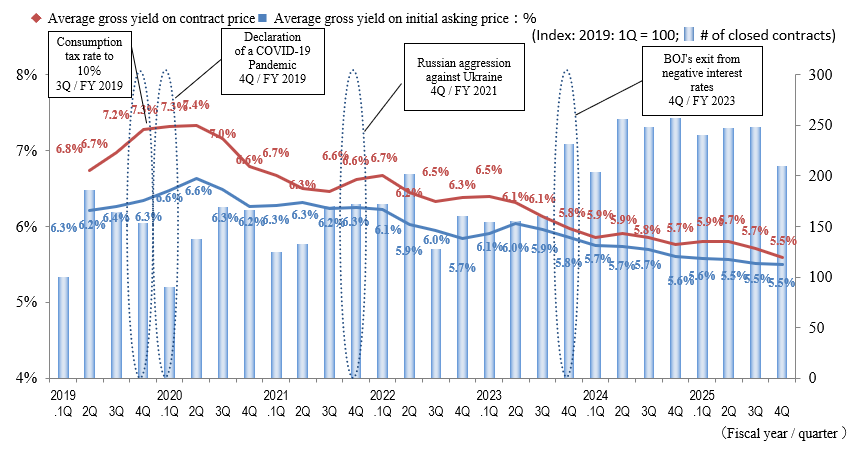

*Figures in each chart represent indices based on values for 1Q / FY2019 set at 100.

(Average Gross Yield on Contract Price is shown as an index to Average Gross Yield on Initial Asking Price for 1Q / FY 2019 set at 100.)

[Note] The historical data may be revised subsequently due to maintenance carried out from time to time, such as adding newly acquired data.

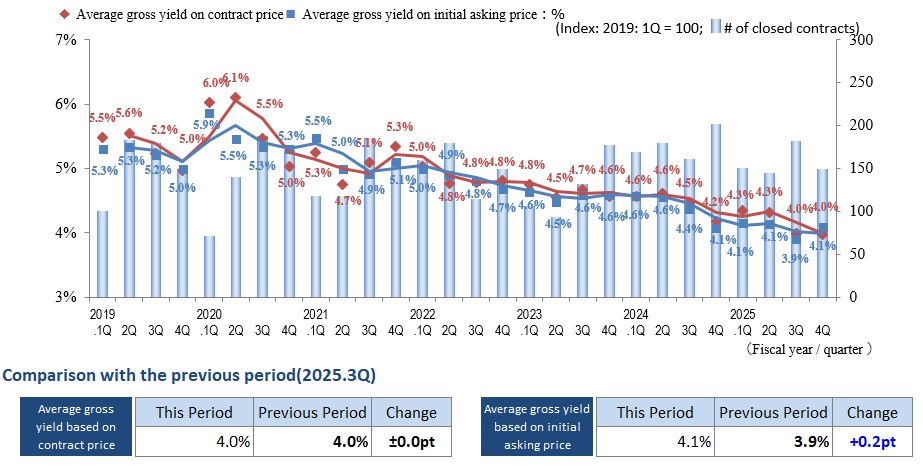

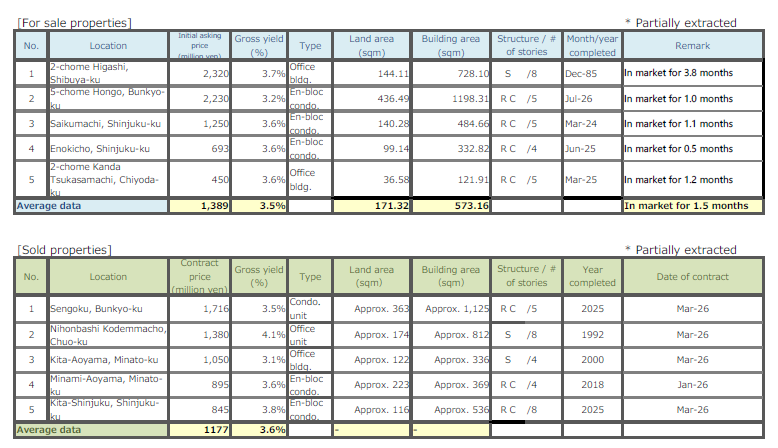

Pick Up Area -Tokyo Central submarket-

◆Movements by Quarter: Average Gross Yield on Contract Price / Average Gross Yield on Initial Asking Price / Number of Transactions

◆Brokered Transactions of Investment Real Estate in the Submarket

In Tokyo Central submarket, the average asking gross yield in 2025 Q4 increased by +0.2 percentage points (indicating a decrease in prices), while the average transaction gross yield remained flat. However, the number of transactions has shown a significant downward trend compared with the same period of the previous year, and this point requires continued close monitoring going forward.

Next, the leasing market in central Tokyo is as follows:

■ Residential: A gradual upward trend in rents continues in Tokyo Central submarket.

■ Office: As in the previous quarter, strong demand continues driven by companies’ needs to improve office environments and locations in order to secure human resources. As supply is also limited, vacancy rates are declining and rents are increasing, particularly for large-scale office buildings.

■ Retail: Inbound consumption continues, and although rents continue to rise mainly for street-front stores in prime central areas, the pace of increase is slowing.

As described above, the leasing market generally continues to perform well across asset classes. On the contrary, concerns that have existed for some time regarding interest rate hikes, as well as the upward trend in management and holding costs—including repair costs driven by rising construction materials and labor costs—together with concerns over the situation in the Middle East, are making the outlook increasingly uncertain.

For income-producing real estate, as rising management and holding costs are unavoidable going forward, in order to maintain or improve net yields, it will be necessary to achieve rent increases that exceed the rise in holding costs. Accordingly, in the evaluation of income-producing real estate, the differentiation between properties that are demanded by tenants and those that are not, is expected to become more pronounced.

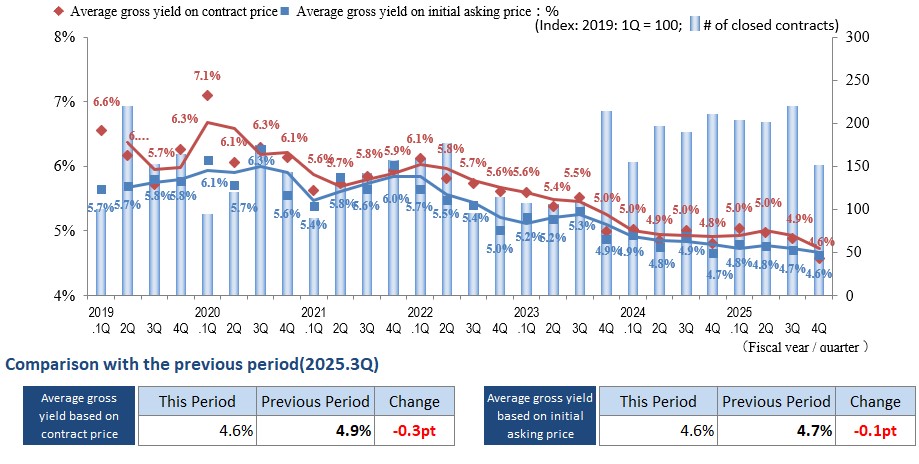

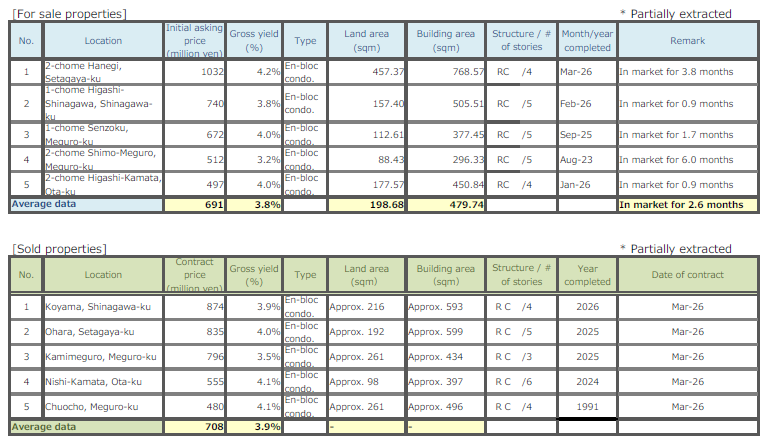

Pick Up Area -Tokyo South submarket-

(*) Tokyo South submarket: Shinagawa-ku, Meguro-ku, Setagaya-ku, and Ota-ku

◆Movements by Quarter: Average Gross Yield on Contract Price / Average Gross Yield on Initial Asking Price / Number of Transactions

◆Brokered Transactions of Investment Real Estate in the Submarket

In Tokyo South submarket, the average asking gross yield in 2025 Q4 was 4.6% (down 0.1 percentage points quarter-on-quarter), and the average transaction gross yield was also 4.6% (down 0.3 percentage points), with both declining (indicating an increase in prices).

This represents the lowest level since 2019, and yields have remained at low levels (with prices at high levels) throughout the year.

The number of transactions decreased significantly compared with the previous quarter; however, it has remained firm on a full-year basis. In addition, the gap between the average asking and transaction gross yields continues to be small, and as this same condition has persisted since the fourth quarter of 2023, it can be said that the market in Tokyo South submarket, based on transaction data, has been progressing in a stable manner.

In Tokyo South submarket, it is expected that stable transactions will continue under relatively strong price settings, supported by solid demand from domestic and overseas high-net-worth individuals for properties that possess the three elements of location, specifications, and future potential.

On the other hand, from January to March 2026, the market has entered a phase in which upward pressure on interest rates, triggered by the policy rate hike at the end of the previous year, has begun to permeate the market. In addition, due to expectations of further rate hikes and concerns over increased borrowing burdens, a certain degree of uncertainty remains in the real estate financing environment. Furthermore, construction costs continue to remain elevated due to high labor costs and material prices, and these continue to be cited as factors of concern.

Going forward, while a stable transaction environment is expected to continue for the time being, as the impact of rising interest rates gradually becomes apparent, there is a possibility that downward price pressure may arise for low-yield properties and properties with challenges in profitability. As a result, the market is expected to shift into a more selective phase.

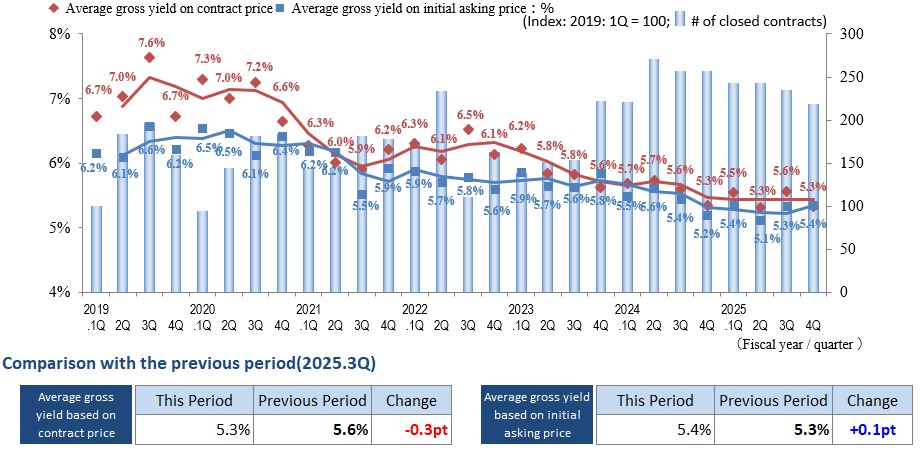

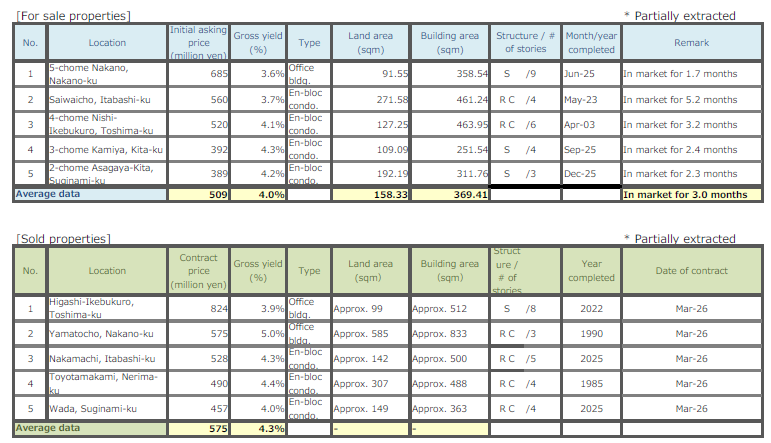

Pick Up Area -Tokyo North / West submarket-

(*) Tokyo North / West submarket: Suginami-ku, Nakano-ku, Nerima-ku, Toshima-ku, Itabashi-ku, Kita-ku, and Taito-ku

◆Movements by Quarter: Average Gross Yield on Contract Price / Average Gross Yield on Initial Asking Price / Number of Transactions

◆Brokered Transactions of Investment Real Estate in the Submarket

In Tokyo North / West submarket, the average transaction gross yield in 2025 Q4 was 5.3% and the average asking gross yield was 5.4%, and when viewed over the past year, both can be said to have remained generally flat.

Regarding transaction volume, it has continued a gradual downward trend since peaking in 2024 Q2, reaching a level comparable to that of 2023 Q4.

While the levels of asking prices and transaction prices have been maintained and there have been no significant changes in supply and demand, factors such as a decrease in newly listed properties and an increase in long-listed properties may be contributing to the gradual decline in the number of transactions.

Prospective buyers continue to place importance not only on yield levels but also on individual factors such as rent levels, occupancy rates, and repair histories, and selection based on comprehensive profitability is being carried out. As a result, there are cases where properties located near train/subway stations, relatively new, or in areas where stable rental demand can be expected, are transacted within a relatively short period of time.

In contrast, for properties where there is room for improvement in rent settings, those that contain vacancy risk, or cases where the asking price deviates from market levels, the number of inquiries tends to be limited, and the trend of prolonged sales periods continues. In this way, although no major price fluctuations are observed in the overall market, it is inferred that differences in competitiveness among individual properties are becoming more pronounced than before.

As a result, while liquidity is secured for properties with appropriate pricing and supported profitability, there are also phases in which a review of sales strategies is required for other properties, and it is necessary to continue closely monitoring real estate market trends going forward.

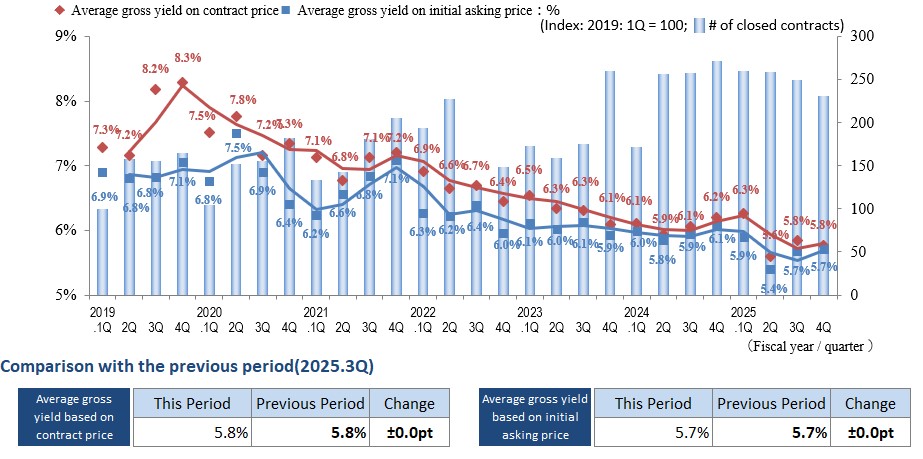

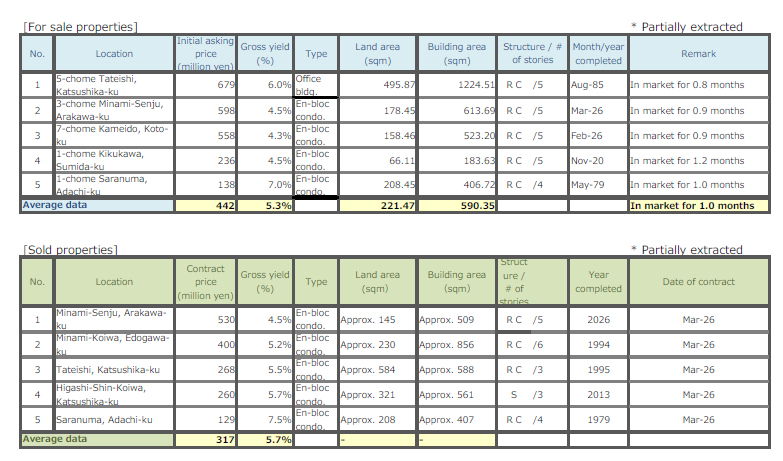

Pick Up Area -Tokyo East submarket-

(*) Tokyo East submarket: Koto-ku, Sumida-ku, Arakawa-ku, Edogawa-Ku, Katsushika-ku, and Adachi-ku

◆Movements by Quarter: Average Gross Yield on Contract Price / Average Gross Yield on Initial Asking Price / Number of Transactions

◆Brokered Transactions of Investment Real Estate in the Submarket

In Tokyo East submarket in 2025 Q4, both the average transaction gross yield and the average asking gross yield stood at 5.8%, remaining flat compared with the previous quarter, and yield levels remained stable.

However, this flat trend does not indicate market equilibrium or the conclusion of price adjustments, but is considered to reflect the fact that, as investors’ decision-making criteria diversify, the characteristics of individual properties and changes in the external environment are beginning to exert a stronger influence.

In the macro environment, the continuation of the interest rate rising phase has impacted investors’ expected yields, and the increase in financing costs has led to more cautious acquisition decisions. In addition, while rising construction costs are making the profitability of new supply more challenging, there are also signs that the relative value of existing stock is being re-evaluated. Furthermore, capital inflows into risk assets continue against the backdrop of rising stock prices, and among some investors, comparisons with asset classes other than real estate are progressing, indicating a growing awareness of optimizing capital allocation.

Looking at individual trends within the area, demand remains firm for properties such as relatively new buildings, those located near stations, and properties in redevelopment areas where stable future cash flows can be expected, and there are cases where transactions are concluded even in lower yield ranges.

On the other hand, for properties with longer building age or those lacking locational advantages, investors’ yield requirements are rising, and a cautious approach to pricing continues to be required.

In addition, for properties with aggressive asking price settings, there is a tendency for longer lead times to transaction, and combined with the decline in the number of transactions compared with the previous quarter, it can be observed that investors’ selective stance is becoming even more pronounced.

While it is not possible to determine the overall direction of the market based solely on the results of this quarter in which yields remained flat, external factors such as interest rate trends, trends in construction costs, and fluctuations in the stock market have a significant impact on investment decisions. Accordingly, it is necessary to continue monitoring transaction trends while closely observing these factors going forward.

Pick Up Area -Yokohama / Kawasaki region-

(*) Yokohama and Kawasaki region: Yokohama city, Kawasaki city

◆Movements by Quarter: Average Gross Yield on Contract Price / Average Gross Yield on Initial Asking Price / Number of Transactions

◆Brokered Transactions of Investment Real Estate in the Submarket

In Yokohama / Kawasaki submarket, the average yields for both asking and transaction prices in 2025 Q4 declined slightly, reaching the lowest levels since the start of the statistical record (indicating an increase in prices).

Although the number of transactions was the lowest in the past two years, a substantial number of transactions are still being conducted, and it can be said that the market has continued to remain active. It will be important to watch whether transaction volume will recover or decline from the next quarter onward.

While there are many investors searching primarily in the Yokohama / Kawasaki area, there are also a certain number of buyers who have begun to consider this area due to its relatively lower unit prices and higher yield potential compared with central Tokyo. However, in making investment decisions, greater caution is being exercised in terms of factors such as distance from train/subway stations and surrounding environments, and a polarization trend between central and suburban locations continues to be observed within the area.

The rise in construction costs continues to be significant, and although there is an upward trend in rents, there are many areas where land development (such as site preparation) is required due to topographical conditions, resulting in cases where it is difficult for developers to undertake projects. In particular, prices for small-scale development sites and irregularly shaped land—where the burden ratio of construction costs tends to be high—are showing a weakening trend.

Meanwhile, stock prices have continued to reach new highs, at one point exceeding JPY 60,000, while uncertainty persists due to rising interest rates and inflation. The previously surging second-hand condominium market in central Tokyo has begun to show slight signs of weakness, with some segments showing a downward trend.

The timing of stabilization in the Middle East situation will also be a key factor going forward, and it remains necessary to continue closely monitoring changes in domestic and international monetary policies and economic conditions.

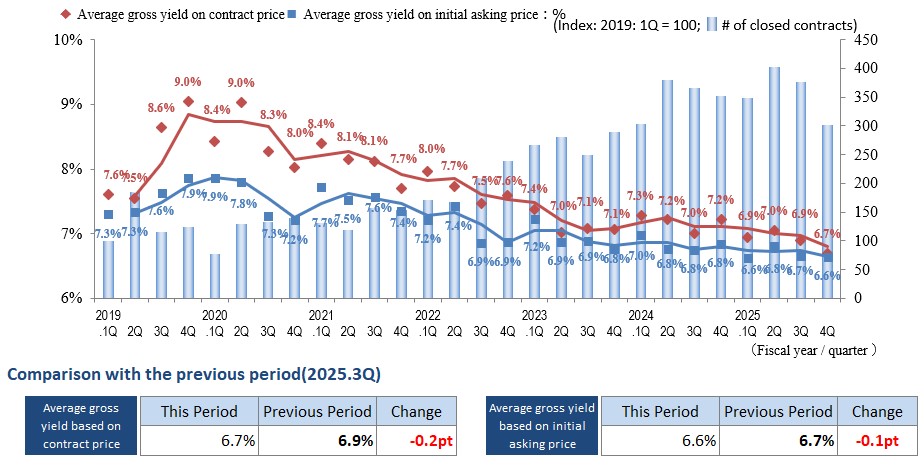

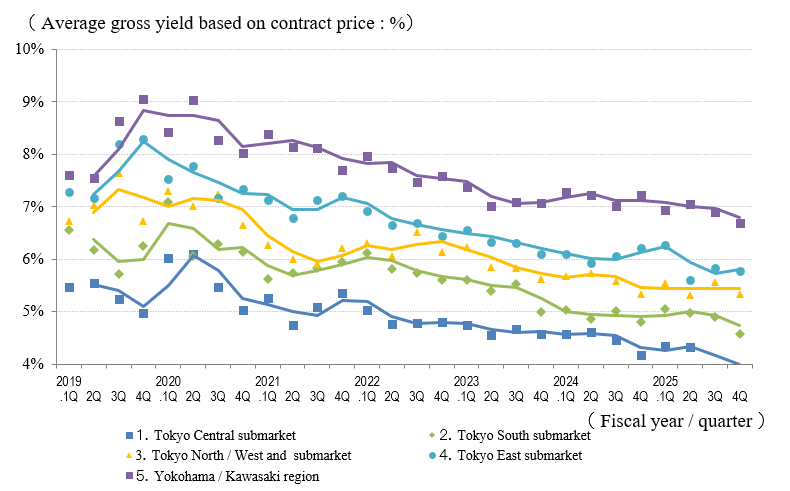

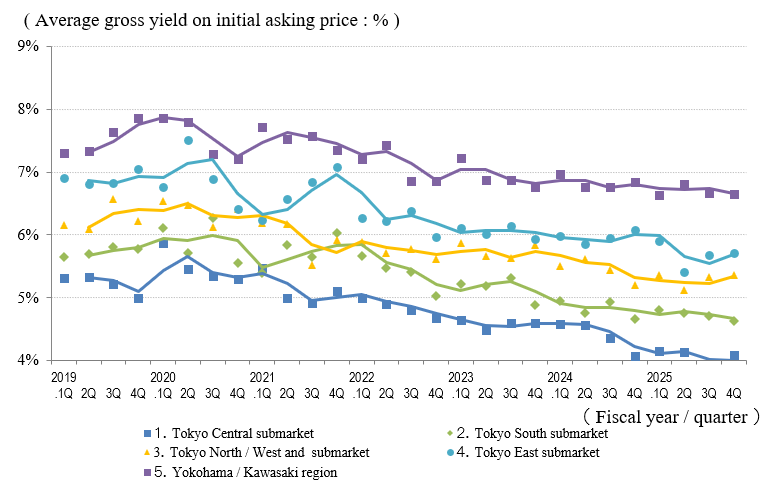

General overview

◆Movements by Quarter: Average Gross Yield on Contract Price / Average Gross Yield on Initial Asking Price / Number of Transactions for the 5 Areas

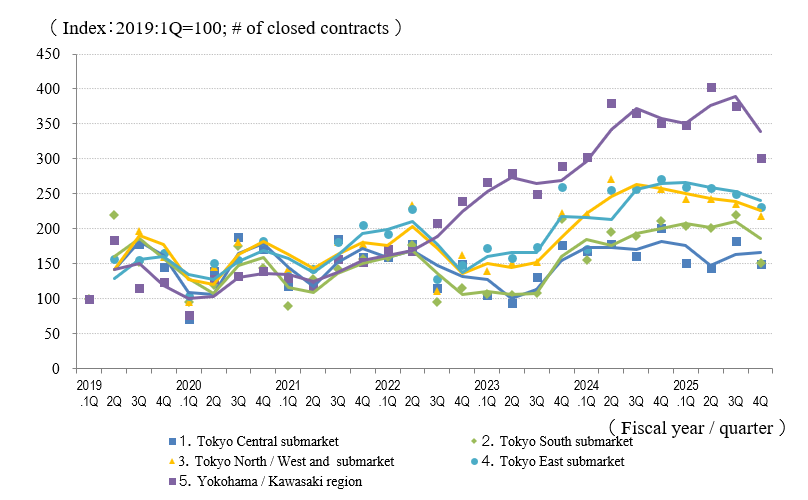

◆Movements in Number of Transactions by Area

◆Movements in Average Gross Yield on Contract Price by Area

◆Movements in Average Gross Yield on Initial Asking Price by Area

The investment real estate market in 2025 Q4 showed a generally flat trend in average yield levels, presenting a superficially stable appearance. On the other hand, a declining trend in the number of transactions has been observed across all areas, and this can be understood as a phase in which the selective stance of investors, which became evident in Tokyo East area in Q3, is spreading and permeating into other areas.

Particularly in Tokyo Central area, while transaction yields remained flat, the number of transactions decreased significantly compared with the same period of the previous year, indicating signs of a shift away from the previously robust level of transaction activity. In Tokyo South area, the average yield reached 4.6%, the lowest level since 2019, and capital concentration into highly competitive areas has become increasingly pronounced against the backdrop of demand from domestic and overseas high-net-worth individuals. It can be considered that, for the market as a whole, a transition toward a phase emphasizing “quality” is steadily progressing.

With respect to the external environment, in addition to the continued permeation of upward pressure on interest rates triggered by the BOJ’s policy rate hike at the end of the previous year, multiple factors influencing investment decisions are becoming increasingly layered, including expectations of further rate hikes, geopolitical risks such as the situation in the Middle East, and the reallocation of capital against the backdrop of rising stock prices. As a result, perspectives that assess not only gross yields but also net yields and medium- to long-term profitability are becoming more important than ever.

We, the Solutions Business Division of Mitsui Fudosan Realty, will leverage our nationwide information network, advanced expertise, and prompt and precise execution capabilities to accurately capture changes in the market environment. Through analysis and proposals aligned with these changes, we will provide optimal solutions that are tailored to each client’s investment strategy and maximize the potential of real estate.

Please feel free to contact us.